Summary

This exhibit presents two sequential communications that demonstrate intentional delay, concealment of renewal documentation, and fraudulent re-characterization of agency authority. Together they establish a textbook instance of wire fraud and conspiracy to defraud under 18 U.S.C. §§ 1343 & 1349.

Exhibit Sequence

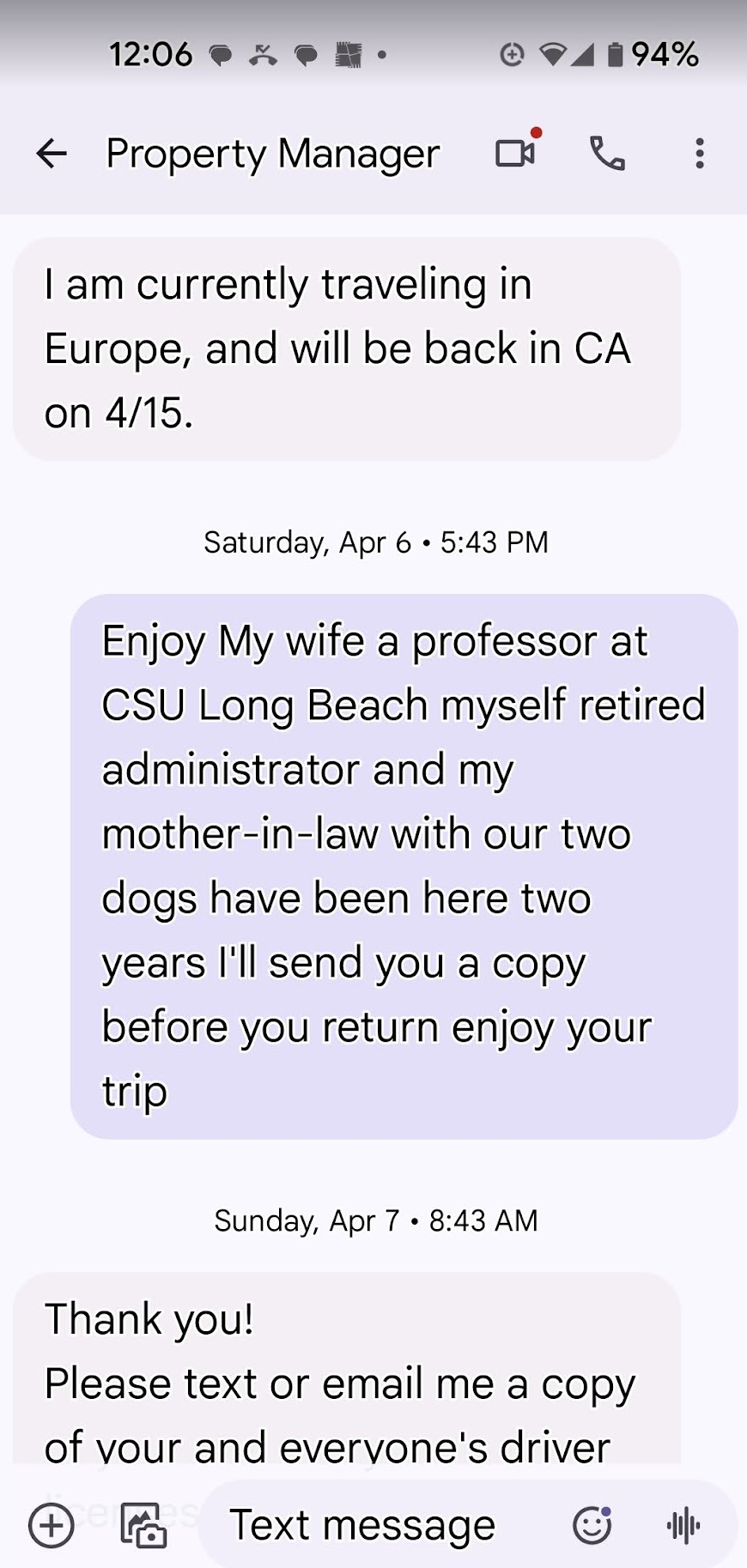

1️⃣ Original Owner Message — April 6-7 2024

The owner explicitly stated they were “traveling in Europe” until April 15 2024 and invited the tenants to “enjoy your trip.” The tenants replied courteously and reaffirmed two-year residency, dogs approved, and intent to sign again. Under California Civil Code § 1636, that exchange forms a continuing intent to renew, awaiting only execution. The delay placed the renewal past the tax-filing date, aligning with later financial concealment motives.

2️⃣ Sudden Appearance of New “Manager” — post-April 15 2024

The following week, Hanson Le introduced himself via text as “a new property manager for Phat Tran,” even though the renewal process was already active and under the owner’s control. This misrepresentation over interstate digital networks constitutes a wire-fraud act because it transmitted a false statement of agency authority for financial gain — rerouting rent into private accounts outside Berkshire Hathaway’s trust ledger.

Legal Analysis

- Predicate 1 – Wire Fraud (18 U.S.C. § 1343): use of electronic communication to obtain property by false pretenses.

- Predicate 2 – Conspiracy (18 U.S.C. § 1349): coordination between owner and agent to delay renewal until control could shift to a private collection channel.

- Predicate 3 – Extortionate Scheme (18 U.S.C. § 1951 – Hobbs Act): threat of eviction following manufactured default.

- State Corollary: Cal. Penal Code § 470 (forgery), § 484 (theft by false pretense), and Civ. Code § 1942.5 (retaliatory eviction).

“Hi Michael, I am Hanson, a new property manager for Phat Tran…” — Text message introducing false agency immediately after owner’s tax-day return.

The juxtaposition of the April 6–7 owner conversation and Hanson Le’s subsequent self-appointment shows a coordinated plan: hold the renewal until after the owner’s return, then introduce a third party to alter financial routing. This sequence fulfills the RICO “pattern” requirement — at least two related predicate acts within a 10-year span serving a common illicit objective.

Why It Matters

No legitimate reason existed for delaying a DocuSign renewal or appointing a “new property manager.” Any genuine manager could have authorized maintenance (dishwasher repair) or accepted rent payments. Instead, the defendants used the delay to re-engineer contractual control, misappropriate payments, and evict a performing tenant under false pretenses. This evidence is a direct link between communication fraud (wire), forged contracts (mail), and monetary conversion — the classic triad supporting federal RICO jurisdiction.